Tech earnings in focus, PMIs and BoC up next

Headlines

* US Treasury yields fall as markets eye earnings and data

* Yen gains for a second day as traders look to BoJ meeting next week

* Wall Street broadly flat, USD attempts to break higher

* Google parent Alphabet beat estimates, Tesla missed on EPS

FX: USD found a small bid as prices tried to get above the 200-day SMA at 104.37. FX markets are relatively muted with the Biden news not unexpected and summer market light liquidity.

EUR slid below support. Focus is on today’s PMI data with a preview below. Traded volatility has been very low recently. An ECB official said September is “more convenient” for ECB decision making.

GBP lost ground but tried to keep hold of support around 1.29. Prices printed at a one-year top at 1.3044 last Wednesday. The March cycle high sits at 1.2893.

USD/JPY outperformed once more as prices dropped to next support around 155.71. A senior Japanese politician added to pressure on the BoJ to keep hiking rates with “growing unease” about policy to boost the yen. Its next meeting is July 31.

AUD fell sharply for a seventh straight day below the halfway point of the 2024 decline at 0.6616. This losing streak hasn’t been seen in 11 months. The kiwi also underperformed, sliding to lows last seen in early May. The antipodeans have struggled after the surprise China rate cut on Monday. USD/CAD pushed higher for a fifth consecutive day near to previous resistance above 1.38 ahead of the BoC rate decision. Another 25bps is virtually fully priced.

US Stocks: US markets were relatively muted with disappointing earnings from household names, but eyes on Tesla and Alphabet earnings released after the close. The benchmark S&P 500 closed 0.20% lower at 5,553. The tech laden Nasdaq 100 finished down 0.20% at 19,783. The Dow Jones finished 0.19% off at 40,337. Tesla was down around 2% after the closing bell, after reporting disappointing earnings as revenues rose 2%. Alphabet met expectations but missed on YouTube ad revenue. The small cap Russell 2000 settled over 1% higher. This continued the theme of rotation out of large cap favoured tech and growth stocks into more unloved and smaller companies. United Parcel Service, seen as a bellwether for the global economy, slumped after missed earnings on soft package delivery demand. Of the 74 S&P 500 companies that have reported quarterly results, over 81% have beaten expectations.

Asian stock futures are in the mixed. Asian stocks were also mixed on Tuesday, with ongoing China frictions battling the tech-led rebound Stateside. The ASX 200 was helped by tech, but energy stock suffered. The Nikkei 225 couldn’t really sustain its opening burst with the firmer yen impeding more upside. The Hang Seng and Shanghai Composite were subdued with markets wanting more from the PBoC and their recent short-term funding rate cuts.

Gold printed a narrow range day, holding around initial support/resistance at $2404. Treasury yields were modestly lower, but the dollar found some support.

Day Ahead – PMIs and BoC Meeting

Eurozone PMI data could see mild softness as the composite figure nears the crucial 50 expansion/contraction marker. But both manufacturing and services are expected to tick very marginally higher. Attention will be on whether any political uncertainty has fed into the data, while prices paid are always watched to guide on inflation. There are a lot of economic releases between now and the ECB September meeting, but markets are pretty convinced the bank will cut rates again at that gathering. The UK PMIs will also be eyed as the Labour landslide could give a lift to the figures. Next week’s BoE rate decision is on a knife edge with around a 44% chance of a rate cut.

Markets are much more convinced the BoC will go through with a back-to-back 25bps rate reduction at its meeting later today. Recent data has cooled with inflation easing and a soft June jobs report. The latest business outlook survey pointed to inflation continuing to fall over the coming year. Traders expect at least two more rate cuts this year. The latest MPR will also give us a good gauge on how the bank expects the economy to perform.

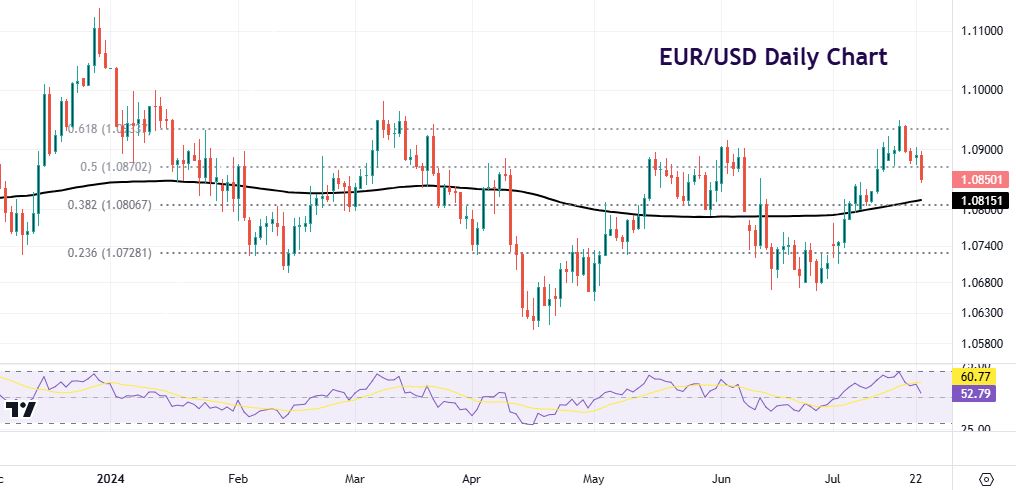

Chart of the Day – EUR/USD loses near-term support

EUR/USD traded volatility remains exceptionally low. There is still a lot of data between now and the September ECB meeting, so the PMI release may not have too much sway on market pricing. Inflationary developments and comments from ECB officials will also act as a guiding force for that meeting on the euro, which currently assigns around a 64% chance of a cut.

The world’s most popular currency pair traded below 1.0870 yesterday, the 50% retracement level of this year’s decline. The 200-day SMA sits at 1.0815 with the next Fib level at 1.0806. Last Wednesday’s top sits at 1.0948, just above the 61.8% Fib level at 1.0933.