Quiet, cautious trade ahead of major risk events

Headlines

* Mixed US jobs data with soft headline but unchanged internals

* US Dollar trades in a narrow range after prior day breakdown

* BoC set to restimulate economy with June rate cut

* Gold dips but still holds recent support above $2300

FX: USD rebounded but the recent technical breakdown remains intact. Job vacancy (JOLTS) data showed that the number of job openings shrank for the second month in a row, setting a new three-year low amid further signals of the labour market cooling. But the quits rate – which is known as a good leading indicator of wage inflation – stayed unchanged at 2.2% for the sixth straight month.

EUR made a fresh six-week high at 1.0916 before pulling back below the figure. German unemployment rose, modestly hurting the single currency. Focus is on Thursday’s ECB meeting. A rate cut is baked in so what President Lagarde says about July and after the summer will be key for markets.

GBP hit a new cycle high at 1.2817, a level not seen since the middle of March. But prices fell and eventually settled below 1.28. There is little UK news apart from election noise.

USD/JPY turned lower again as the 10-year Treasury yield continued down into strong support around 4.33%. The major has lost over 1.5% in two days as a big squeeze on funding currencies turns. USD/JPY has hit the 50-day SMA at 154.76. It hasn’t closed below this indicator since March.

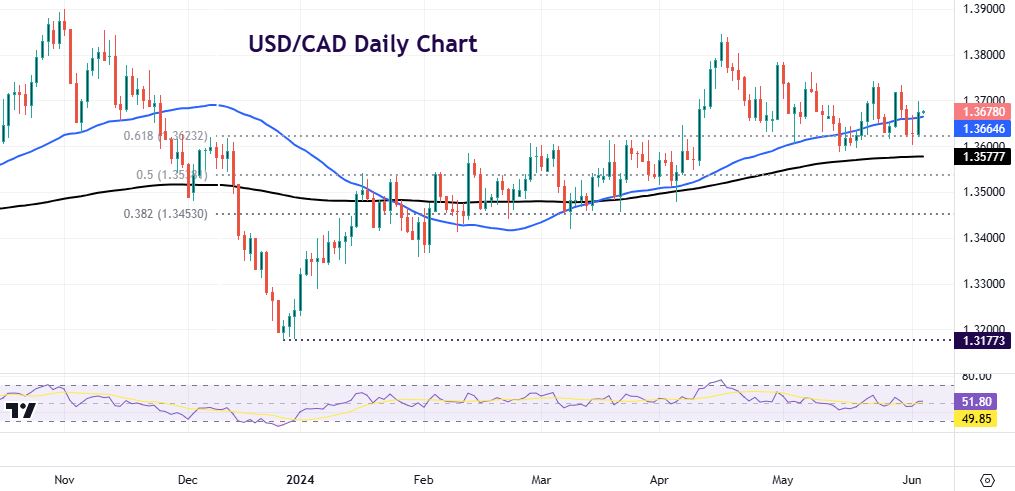

AUD struggled again at resistance around 0.67. USD/CAD moved above its 50-day SMA at 1.3664. Attention is on the BoC meeting today.

US Stocks: Indices closed mixed again in relatively rangebound markets. The S&P 500 finished higher by 0.15% at 5,291. The Nasdaq 100 settled 0.29% up at 18,655. The Dow closed in the green by 0.36% at 38,711. Markets were fairly cautious with some choppiness around the US jobs data. Tesla CEO Musk said his current best guess for Nvidia purchases by Tesla is $3-4 billion this year. Nvidia closed on its highs at another fresh record high. Tesla continues to struggle below $180.

Asian Stocks: APAC futures are mixed. Asian stocks traded mixed with the tone moderately lower. The ASX 200 saw gains in gold names but losses in energy. The Nikkei 225 underperformed with energy and autos falling. The latter fell after a safety test scandal. China stocks were mixed with Hong Kong holding modest gains. The mainland was flat trading in a tight range.

Gold fell over 1%. The 50-day SMA sits at $2334.

Day Ahead – Australia GDP, BoC Meeting

Economic activity in Australia is expected to have slowed to 1.2% in Q1 from the prior 1.5% y/y and 0.2% q/q. Consumption was likely subdued reflecting the ongoing constraints from high inflation, interest rates and increased taxes. Retail sales figures show consumers continuing to curtail spending. Economists say that residential investment is also likely to have contracted, given the supply constraints facing Australia’s housing market. That said, resilience in business investment and public spending might offset the above. Prices in AUD/USD have tracked sideways between 0.66 and 0.67 for the last three weeks. The major recently hit resistance again around 0.67.

The Bank of Canada is now expected to cut rates by 25bps to 4.75%. This follows weak Q1 growth and solid signs of disinflation continuing. Unemployment has risen above 6% while wage growth is contained and core CPI below 3%. Attention will be on any guidance the BoC and Governor Macklem give on future rate cuts. Data since the last meeting does point to multiple cuts through the second half of the year.

Chart of the day – USD/CAD sideways for now

The nagging doubt is that the BoC hasn’t explicitly signalled its intention to cut rates at today’s meeting. The markets have priced in a move, but it seems holding rates steady would support the bank’s aim to be transparent and keep up their effort on forward guidance.

USD/CAD tested minor support in the low 1.36s yesterday but shied away from a push to test key support just below the figure. Prices have moved higher with bulls hoping to break decisively above themed-1.37s on a more dovish than expected BoC. Strong support sits around 1.36 with the 200-day SMA at 1.3577.