Markets positive after Trump assassination attempt and dovish Powell

Headlines

* Powell indicates Fed won’t wait until inflation is down to 2% before cutting rates

* Goldman profits surge 150% from year ago on Wall Street rebound

* Bitcoin rallies as Trump optimism powers crypto after shooting

* Bank of Canada surveys show subdued inflation expectations

FX: USD started the week consolidating near strong support around 104.10, but below the 200-day SMA at 104.43. The Trump attempted assassination has not had a big impact on markets, but it has lifted his odds of becoming President again. The 2.0 version is expected to be inflationary with tariffs, tax cuts and immigration controls. That would hit the bond market and potentially offer support to the dollar. Fed Chair Powell indicated a rate cut is coming with increased confidence with recent inflation readings and falling closer to target.

EUR popped up to a high of 1.0922 before paring gains below the big figure. The ECB meeting may not offer much, with the September meeting much more important. A rate cut is very likely with markets continuing to price in well above a 50% chance of a second cut in December. Today’s German ZEW index is expected to show a further loss of momentum in leading activity indicators.

GBP made more fresh one-year highs at 1.2995. It’s a big week of UK data with the last CPI and wage growth numbers ahead of the 1 August BoE meeting. Market bets see traders flipping a coin as to whether the MPC cut rates then or not. These odds have been reined in since we heard relatively hawkish noises last week from Chief Economist Pill.

USD/JPY fell to 157.15 before finding support at the 50-day SMA at 157.83. The 10-year US Treasury steadied moving above 4.2%. The midpoint of the May low to July high sits at 156.90.

AUD stumbled modestly as prices struggle to make any headway above 0.68 on subdued China data. Focus will be on the jobs report released on Thursday. USD/CAD moved further away from the 200-day SMA at 1.3594. Eyes are on the Canada CPI data released later today. See below for more detail.

US Stocks: US markets closed in the green. The benchmark S&P 500 made a fresh intraday record high, but settled just below 5,666, 0.28% higher at 5,631. The tech heavy Nasdaq 100 finished 0.27% up at 20,386. The Dow Jones closed 0.53% stronger at 40,211. Energy and financials gained more than 1.4% with utilities the biggest loser. Once again, we saw rotation and outperformance in small caps and value stocks with the Dow and Rusell 2000 beating the other indices. Goldman Sachs beat on EPS, overall revenue and Fixed Income sales and trading revenue. The stocks broke higher and finished 2.57% higher, nearing the $500 mark. Apple revealed Indian revenue increased 33% nearing $8 billion. Morgan Stanley raised it price target.

Asian stock futures are mixed. Asian stocks were mixed after a slew of China data included disappointing GDP, retail sales and house prices. The ASX 200 rose above 8,000 for the first time with tech and telecoms leading the gains. The Nikkei 225 was closed for Marine Day. The Hang Seng and Shanghai Composite were mixed with the Hang Seng hit by tech and property losses amid weak China data.

Gold hit levels last seen when prices spiked higher to the all-time high at $2450 in May. Bullion pulled back intraday from its top at $2439. It seems only a matter of time before the record high is challenged.

Day Ahead – US Retail Sales and Canada CPI

Headline retail sales are expected to print unchanged and marginally lower than the May number. The core is predicted to tick one-tenth higher, while the control metric, seen as the best gauge for GDP consumer spending, will be watched. Lower gasoline prices, given the sales number is a dollar value figure, will likely be a key driver of the data.

Canada CPI will be key for the BoC decision next week. The inflation print in May was hotter than expected with the core measures stuck at the upper end of the target of 1 to 3%. The job market was very weak with the unemployment rate continuing to rise, though strong wage gains were seen again for a second straight month.

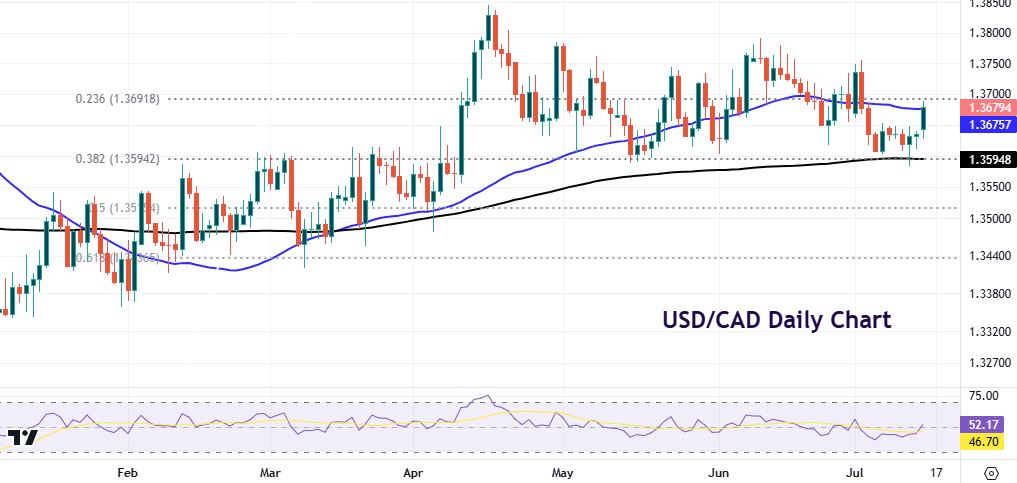

Chart of the day – USD/CAD finds support

USD/CAD has been relatively quiet trading between 1.36 and 1.38, give or take, for the past few months. Prices look to have found support at the 200-day SMA at 1.3594 and a long-term Fib level (38.2%) of the December to April move also at 1.3594. The major moved higher yesterday up to the 50-day SMA at 1.3675.

Canada CPI will be key in determining whether we see back-to-back rate cuts by the BoC. Markets currently price in around 17bps of easing for the July meeting, which implies a 68% chance of a rate reduction. Soft data could see the major push up above 1.37 while sticky numbers will have to battle that strong support around 1.36.