Bets on rate cuts reduced again as USD surges

Headlines

* Yen wavers after media reports suggest the BoJ will end NIRP

* Key US data pours more cold water on rate cut hopes

* Treasury yields surge as traders prep for Dot Plot with three cuts in question

* Oil hits four-month high above $85 as IEA predicts market deficit

FX: USD surged higher breaking to the upside after consolidation below 103. Hotter-than-expected PPI, soft US retail sales and below-consensus weekly initial jobless claims data all added to Tuesday’s strong CPI figures. Eyes are on the 200-day SMA in the Dollar Index at 103.69 if bulls can sustain this advance north.

EUR suffered its worst day since the start of February. The world’s most popular major sliced through the 50% level of the December/February sell-off at 1.0916 and below 1.09. Next level of support is 1.0875. There were a lot of ECB officials on the wires. Dovish remarks from Stournaras grabbed thew headlines who said the needs to be cutting soon and 4 cuts in 2024 seems reasonable.

GBP dipped below 1.28 to a low of 1.2731. There was little UK news. The latest Reuters poll sees the BoE cutting rates by 50bps to 4.75% in the third quarter.

USD/JPY finished higher as US Treasury yields shot higher. There was much media speculation about the upcoming Rengo wage talks and the potential ending of NIRP. The 50-day SMA sits at 148.38.

AUD struggled and fell back to the midpoint of the Q4 rally at 0.6571. Attention turns to next week’s RBA meeting. USD/CAD popped higher and back above the 200-day SMA and 50-day SMA at 1.3479/80. Resistance is 1.3538.

Stocks: US equities were subdued again though managed to climb off their lows in the final hours of trading. Hotter input prices raised the prospect of less cuts on the year. The broad-based benchmark S&P 500 closed 0.29% lower at 5,150. The tech-dominated Nasdaq 100 slid 0.30% to finish at 18,014. The Dow Jones settled 035% up at 38,905. Real estate was the big laggard with energy the main winner. Stock wise, Nvidia and Tesla led the declines losing 3.24% and 4.12% respectively. The latter is now down over 34% on the year so isn’t just underperforming as a member of the Mag 7, but also the wider S&P 500 index. Analysts have been cutting their ratings and price targets citing weak consumer demand and slower production in North America and Europe.

Asian futures are in the red. APAC stocks traded mixed after similar performance on Wall Street. The Nikkei 225 traded indecisively while the ASX 200 was muted as gains in commodity-related sectors were overshadowed by tech and financial losses. The Hang Seng was varied amid tech-related headwinds after the US House banned TikTok.

Gold declined as yields surged higher. It’s been a volatile and whippy week with US CPI and PPI data. The market reaction was mixed until yesterday’s much stronger than expected PPI figures hurt Treasury prices and boosted the dollar. The previous spike top back from December last year is $2148. Less than 75bps of rate cuts are priced in for 2024 now. This was above 90bps before NFP and US CPI.

Day Ahead – Japan Wage Negotiations (First tally from Rengo)

It’s a key risk event for the Bank of Japan and their meeting next week. Indeed, BoJ Governor Ueda recently mentioned the relevance of data, pointing to today’s wage talk results. Rengo, Japan’s biggest labour union, release their first tally of pay deals today. The Federation wanted more than 5%, before actually guiding that their average being sought was 5.85%. This is way above the 3.8% agreed upon in 2023.

That matters hugely as rate hike expectations have ramped up recently with a high chance of a historic move soon. Other large corporates like Toyota and Panasonic have promised workers the largest pay rise in more than three decades. If solid wage growth boosts private consumption, the end of NIRP is nigh. That should see strong support for JPY. The press release is expected around 16.15 Tokyo time (+9 GMT).

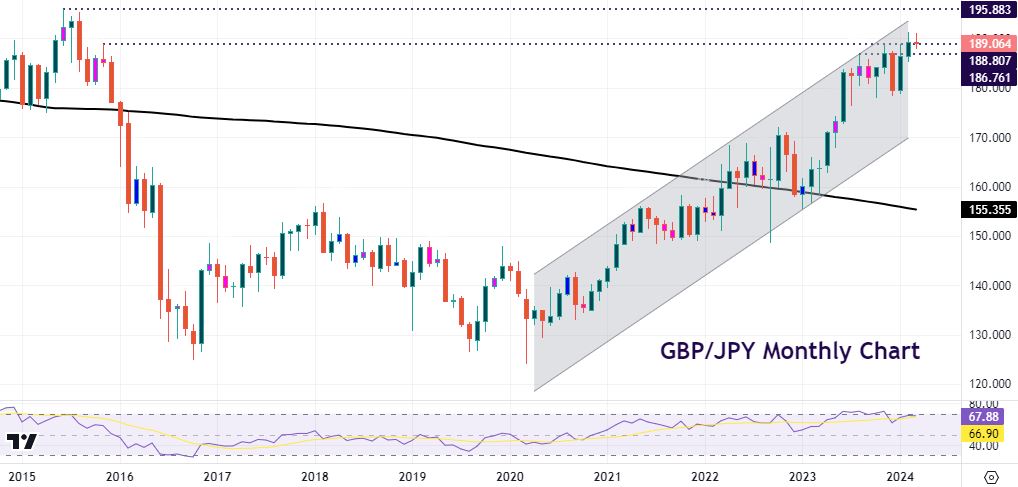

Chart of the Day – GBP/JPY off recent nine-year highs

GBP/JPY has been in a strong long-term uptrend since 2020. Support was found around 124/125. Prices have moved up since, in more or less a series of higher highs and higher lows. The minor recently found resistance 191.18/31 in late February and early March. The cross looked to be rolling over but found support at the November 2015 high at 188.80.

A very strong Rengo wage tally could bid up the yen and see this pair break down through initial support at 187.97. We note negative divergence on the monthly chart. Next support below is the August 2023 top at 186.76. The 200-day SMA is 184.16. Next week sees the BoJ meeting on Tuesday, followed by UK CPI a day later and the BoE meeting next Thursday.